Space SPACs

SPAC your bags, we're going to space

Until fairly recently, there was really no opportunity for public investors to invest in the companies that would typically be categorized as belonging to the “New Space” industry. Yes you could invest in Lockheed Martin, Boeing, or a number of other legacy space companies, but not the ones driving much of the most recent buzz in the sector. Thats changing in real time though as a number of these younger companies are hitting public markets, not through a traditional IPO process but instead through a vehicle popularized more recently, a SPAC.

By the end of this year there may be ten or more public space companies. In this post I’ll talk about the below topics regarding how SPACs are impacting the commercial space industry:

What is a SPAC

What Space Companies have announced SPACs

What does it mean for the industry?

What is a SPAC

Feel free to skip this section if this isn’t new to you.

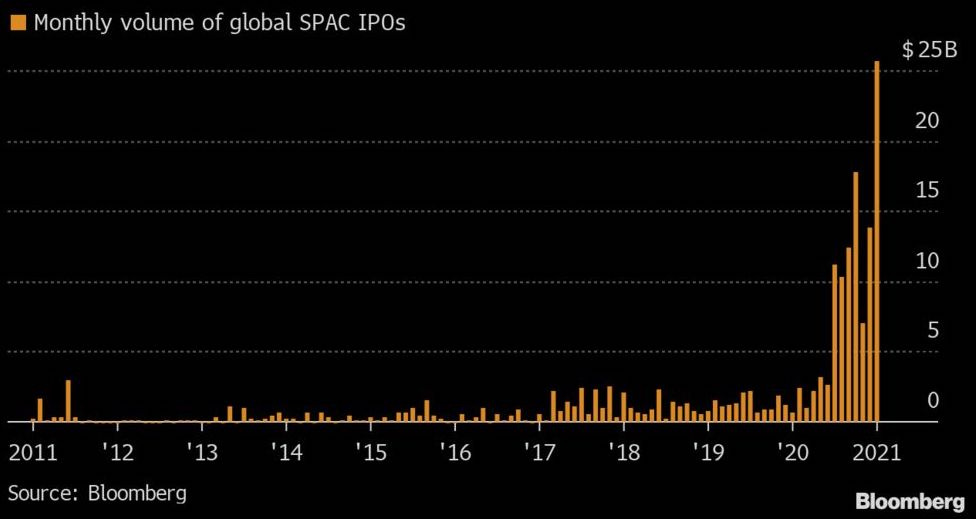

A Special Purpose Acquisition Company (a.k.a. “SPAC”) is a publicly listed shell company whose sole purpose is to acquire, or merge with, an existing private company, thereby making the private company publicly listed. A SPAC is sometimes referred to as blank check company because until its management team (known as the “Sponsor”) finds a target to acquire, the SPAC itself has no commercial operations. You can think of a SPAC simply as a pile of investors’ money sitting in a savings account that can only be accessed if the Sponsor finds a suitable target to acquire.

The majority of SPACs range between $100 million and $500 million with at least two percent of the funds coming from the Sponsor’s own money. This two percent is used to fund the Sponsor’s acquisition search and gives its team some financial “skin in the game.” After the Sponsor has secured committed investors, they take the SPAC (a.k.a. the pile of money) public via a traditional IPO. Once public, the Sponsor has two years to locate an acquisition target, otherwise the funds are returned to investors, and the Sponsor loses the two percent they personally invested.

Next, assuming the Sponsor finds a company interested in going public via their SPAC, they negotiate terms at which the SPAC will merge with the private company. The private company merges with the publicly listed SPAC and during this process the private company receives the SPAC’s cash and assumes the public listing status in exchange for an ownership stake in the combined business. Once the merger is complete the Sponsor relinquishes their remaining managerial control to the private company’s executives who will operate the newly public company.

After a SPAC merger is announced and before it closes, there are various regulatory and legal topics which must be addressed. The private company and SPAC file an S-4 document with the SEC to disclose to the public information about their history and future planning. Importantly, the SPAC’s shareholder must vote to approve the merger before the deal is closed. The time from announcement of the SPAC merger until closing of the business combination can be as short as three months but typically companies target four to six months for the process.

The SPAC process also often involves a Private Investment in Public Equity or PIPE. Think of the PIPE as additional capital for the deal that the Sponsor raises from institutional investors after locating a target to merge with. PIPE investors like this because they don’t have to tie their money up in the SPAC while the Sponsor seeks a target, yet they get to invest at the same terms as the SPAC investors before the newly combined business becomes publicly tradable. Raising a large PIPE also serves the SPAC because the PIPE investors are typically credible, long-term oriented institutions which can provide credibility to the terms of the merger and legitimacy of the newly public company.

What Space Companies Have Announced SPACs?

Virgin Galactic

SPAC Valuation: $1.5B

SPAC Capital Raised (including PIPE): $774M

SPAC date announced: 7/9/2019

SPAC Merger Closed: Yes

Virgin Galactic, founded in 2004 by Richard Branson, was the first space company to go public via a SPAC back in 2019. They provide suborbital space tourism by sending passengers on a trip up to the edge of space and back, with the mission “to be the spaceline for Earth”. The company merged in 2019 with Social Capital Hedosophia, a SPAC managed by high-profile investor Chamath Palihapitiya. The volatility that comes with being a publicly listed, multi-billion dollar, largely pre-revenue company is excellently exemplified with Virgin Galactic. When its SPAC merger completed in October 2019, the company was valued at around $1.4B. In the 22 months since, the valuation has shot up to over $10B, down to $4B, back up to over $12B and at the time of writing is around $6.8B. Virgin’s June 11th high-profile launch of founder Richard Branson to space was a major event, signaling the organization’s plans to begin ferrying paying customers very soon. If you want to learn more about Virgin’s plans, you can check out my previous post about suborbital space tourism.

Momentus

SPAC Valuation: $566.6M

SPAC Capital Raised (including PIPE): $247M

SPAC date announced: 10/7/2020

SPAC Merger Closed: Yes

Momentus is developing a “space tug” technology, which is a system that carries a satellite from one orbit to another. This is particularly helpful if your satellite reaches space via a rideshare launch, in which you are dropped off in orbit alongside a number of other satellites hitching a ride on the same rocket. In that case, you may need to travel a bit further to reach your preferred orbit and a space tug will help get you there. Momentus announced its SPAC in October 2020 at a $1.2B valuation but faced pushback from the US Department of Defense regarding ownership by its Russian founders, resulting in Momentus being unable attain the licenses to test its technology in space. The pressure resulted in Momentus’s delaying its tests by at least a year and the international owners divesting from the company. Following these challenges, the SPAC merger was revised to a post-merger enterprise value of $700M from the original $1.2B. Recently, Momentus reached a settlement of a $7M penalty with the SEC due to claims that the company and its former CEO misrepresented the readiness of its technology.

Astra

SPAC Valuation: $2.1B

SPAC Capital Raised (including PIPE): $489M

SPAC date announced: 2/2/2021

SPAC Merger Closed: Yes

Astra is building the smallest rocket coming to market in the near term. Its Rocket 3 vehicle is currently capable of lifting 50kg to orbit with plans of expanding that capability up to 500kg in the coming years. When its SPAC merger completed on July 1, Astra became the first small orbital rocket company to be available to public investors. The company has grand ambitions of launching rockets every single day by 2025, eventually at prices as low as $1M per launch (current launch costs are about $3.5M). Astra is already putting the SPAC capital to use and in June announced the acquisition of satellite electric propulsion company Apollo Fusion. The acquisition supports Astra’s efforts to build their own satellite system to vertically integrate both the launch and satellite development process for its customers. Astra claims to have over 50 launches under contract, representing more than $150M in revenue.

AST & Science

SPAC Valuation: $1.8B

SPAC Capital Raised (including PIPE): $462M

SPAC date announced: 12/16/2020

SPAC Merger Closed: Yes

AST & Science is a company looking to launch “a space-based satellite network that allows any phone — without any modification of hardware, software, apps, nothing — to be able to connect directly to satellites” according to its CEO Abel Avellan. The goals of the company are extremely ambitious and the organization’s technology is still in the very early stages of development. AST launched an experimental technology demonstration satellite named BlueWalker 1 in April 2019 and is seeking to send up its next test satellite, BlueWalker 3 in late 2021. Before going public, the company had raised about $120M from strategic investors like Vodafone, Samsung, American Tower, and Rakuten. The company hopes to launch its first production satellites in 2023 which would initiate services around the equator and eventually provide service to over 1.6 Billion people.

Rocket Lab

SPAC Valuation: $4.1B

SPAC Capital Raised (including PIPE): $790M

SPAC date announced: 3/1/2021

SPAC Merger Closed: Yes

Rocket Lab is the most established small rocket company to go public via a SPAC. Rocket Lab began launching satellites to orbit for customers in 2018 and has since been working up to a current launch cadence of about once per month, resulting in 2019 revenue of $48M. The company’s current rocket, named Electron, has the capacity to put about 300kg into Low Earth Orbit at a price of around $7M. Rocket Lab’s SPAC funding will go towards two major projects, the development of its next generation rocket Neutron and its satellite bus system Photon. Neutron will be a medium-class lift vehicle capable of putting up to 8,000kg to orbit and will target the market of launching satellites in batches to specific orbital planes, serving customers looking to deploy satellite constellations.

Redwire Space

SPAC Valuation: $615M

SPAC Capital Raised (including PIPE): $163M

SPAC date announced: 3/25/2021

SPAC Merger Closed: No

Redwire is seeking to become a vertically integrated space infrastructure company and is aiming to do so by acquiring a number of smaller space companies with aligned technologies. A few of these acquisitions have included Made in Space which developed in-space 3D printing technology, Adcole Space which develops satellite components, and Deep Space Systems which supports the development and operations of spacecraft. Some major contracts won by Redwire’s portfolio of companies include developing avionics for Firefly’s lunar lander, a robotic arm for Momentus’s Vigoride space tug, and a 2019 NASA contract to Made in Space for leveraging the company’s manufacturing abilities.

Planet Labs

SPAC Valuation: $2.8B

SPAC Capital Raised (including PIPE): $545M

SPAC date announced: 7/7/2021

SPAC Merger Closed: No

Planet is seemingly the largest-by-revenue space company to announce a SPAC, with growing sales of over $100M. The organization has been around since 2010 and has been one of the pioneers of the usage of small satellites to disrupt industries previously dominated by legacy space companies. Planet Labs operates a constellation of over 200 satellites to take pictures of Earth. The company was created with the mission to image the entirety of Earth every single day and is currently meeting that goal. This rapid revisiting to take pictures of the same spot on the planet every day allows for Planet’s customers to monitor changes and trends taking place on Earth’s surface. Planet has demonstrated steadily increasing recurring revenue, with its Annual Contract Value increasing from $43M in 2016 to $113M expected in 2021, a CAGR of 27%.

Spire Global

SPAC Valuation: $1.6B

SPAC Capital Raised (including PIPE): $265M

SPAC date announced: 2/18/2021

SPAC Merger Closed: Yes

Spire Global was founded in 2012 to provide data and analytics by leveraging a constellation of satellites based in Low Earth Orbit. The company operates a network of over 110 of its Lemur satellites, which utilize multiple sensors that carry out more than one type of function to collect Earth data. One sensor function is radio occultation, which enables the satellites to gather atmospheric weather information by very precisely measuring how GPS signals are refracted as they travel through the Earth’s atmosphere. This refraction is impacted by atmospheric effects that Spire collects and provides as weather data to its customers. The Lemur satellites also carry sensors to receive tracking information from sea-vessels and aircraft, allowing Spire to offer realtime maritime and aviation tracking. Spire recorded $28M in GAAP revenue in 2020.

BlackSky

SPAC Valuation: $1.5B

SPAC Capital Raised (including PIPE): $450M

SPAC date announced: 2/18/2021

SPAC Merger Closed: No

BlackSky was founded in 2013 and is an Earth observation company operating satellites to take images of Earth. The company currently operates five satellites and plans to expand that network to 30 over the comings years. The organization’s goal is to be able to image the entirety of Earth every 30 minutes. This extremely rapid revisit would seek to provide BlackSky’s customers with a “first-to-know” advantage over events unfolding on Earth’s surface. Rather than build BlackSky’s satellites entirely in-house, the spacecraft are made by LeoStella, a joint venture with legacy satellite manufacturer Thales Alenia Space. BlackSky intends to use the funding from the SPAC to “extend BlackSky’s AI/ML analytics platform, expand BlackSky’s small satellite constellation, add additional sensors and data feeds to the BlackSky network and accelerate the Company’s penetration of the commercial market.”

Virgin Orbit

SPAC Valuation: $3.7B

SPAC Capital Raised (including PIPE): $483M

SPAC date announced: 8/23/2021

SPAC Merger Closed: No

Virgin Orbit is small launch company that is an entirely separate entity from the suborbital space tourism company Virgin Galactic. Virgin Orbit uses a unique air launch system where its rocket, LauncherOne, is first carried beneath the wing of a 747 aircraft (nicknamed Cosmic Girl) and dropped from about 35,000 before its engines ignite. LauncherOne has successfully reached orbit on two flights at this point, making it only the second venture-funded small launch company to do so, behind RocketLab.

What Do SPACs mean for the Space Industry?

Generally, the impact of SPACs on the space industry seems to me to be positive, but I don’t say that without some trepidations. On one side, private companies looking to operate in an extremely capital intensive industry (space projects are expensive) get to raise money from a whole new segment of the population that they would otherwise be excluded from. On the other side, public investors get to participate and benefit financially from the innovation taking place in an exciting new industry, instead of those financial benefits only being limited to accredited investors.

That being said, what I think is often said but not always fully appreciated is that SPAC’s do not face the same regulatory restrictions that are involved in going public through other means. A primary example of this is that SPAC’s are able to market to investors their projections for future performance in ways that companies are not allowed to do in a traditional IPO process. Being able to market to public equity investors on forward projections is a massive benefit for the company’s management. However it also means that a company can provide rosy projections to public investors who may not have clarity on how skeptical they should be of those outcomes. Consequently, there is additional burden on the investor to fully understand the risks of putting their money into these companies.

Furthermore, this benefit can become a double-edged sword. While offering mouthwatering projections that are 5+ years away sounds great, public investors will undoubtedly hold companies to their projections and any unexpected miss or delay can rapidly become painful to the stock price.

Additionally, once a sponsor has raised money for a SPAC, there is an intense financial incentive for them to find a private company to merge with. This is because if they don’t find one, they lose the approximately 2% of the funding they themselves put into the SPAC. As a result, even if an ideal private company was not found, there is a possibility that the SPAC’s leadership would move forward with a less-than-ideal merger anyway. As a result I believe that public investors should approach SPACs with increased scrutiny than they might towards companies going public via other means.

We have already started to see the early impact of the opacity of some of these SPAC’s exemplified through the recent troubles with Momentus. In fact, after Momentus and its merging SPAC were fined, the SEC chair Gary Gensler stated “This case illustrates risks inherent to SPAC transactions, as those who stand to earn significant profits from a SPAC merger may conduct inadequate due diligence and mislead investors.”

On the other hand, public investors who have owned Virgin Galactic shares since its SPAC merger closed in 2019 have seen an increase in their stock value of about 200% (at the time of this writing). Without a SPAC, Virgin Galactic may have struggled to raise the funding necessary to start scaling its launch operations and retail investors would have missed out on this upside.

The popularity of SPAC’s has skyrocketed in recent years and we have yet to settle into a new equilibrium so it’s unclear whether this disruption to traditional means of going public is temporary or more permanent. One thing SPAC’s have been able to illustrate is that there is significant interest in the space industry from public investors. At the time of this writing, Virgin Galactic was the 57th most highly traded stock on the New York Stock Exchange, despite not even being in the top 500 largest companies on the exchange.

While it’s too early to tell how all of this plays out, I think the genie is out of the bottle and we’re likely never going to return to a time when New Space companies aren’t accessible to public investors. It marks another new exciting milestone of wider approachability for the space industry and that trend of broader access and transparency is likely to benefit everyone involved.

Additional Reading

Liked this read? Follow me on twitter for more frequent updates on the space world.

Want to read more about satellites? Check my previous post about investment opportunities from the rise of satellite constellations.